inlord 寫道:

Ron & Oneness,

想請教, 以下:

1.Fist State China Growth Fund有I, II & III, 那一個好呢?

2.另外已持有Templeton Asia Growth Fund, 是否仍可考慮買入Allianz GIS RCM Total Return Asian Equipt Fund, 或將資金放到 Fidelity European Aggressive/Growth EUR貨幣

thanks.

sunshine0613 寫道:

Ron, Oneness,

Can I have your advice for future investment?

I have started my fund (excluding MPF) investment as below in Aug 06:

1) Fidelity Funds - European Aggressive Fund 20%

2) First State China Growth Fund 20%

3) Franklin Templeton Asian Growth Fund (ACC) 20%

4) Investec GSF Global Strategic Value (A) (Inc) 40%

Above total lump sum investment of HK$100000 is target for 12% annual return for my 2-year old daughter university education.

On top of the above, I would like to start a monthly investment plan for my retirement (20-25 years later). I plan to invest about $3000 per month. I can accept high risk. What will be good choice for the profile and any recommentation about the fund?

Besides, I have ~ HK$200000 (HK markets shares e.g. #005, 939, 3988) on hands. I need to cash them in the coming 1-2 years time for building house (original resident of NT) together with family members. Should I swap the money from share to fund right at now?

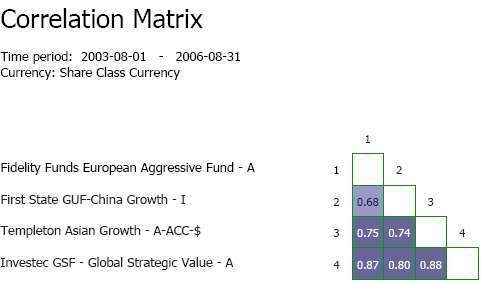

Oneness 寫道:

The funds in your portfolio has very high correlation with each other (see below). Therefore the risk cannot be diversified. You need to rearrange your portfolio to reduce the risk.

Oneness 寫道:

Your shares are all from the banking sector. This share portfolio is therefore not diversified. I would suggest you replace 939 and 3988 with other stocks or funds. 945 is a good choice for the long term.

Ron38 寫道:

不應只重視Correlation在Portfolio 的作用.

Correlation 是可以參考,但更重要的,是個別基金的 '表現' 及 '風險'.

而且,組合方面,每隻基金的'比例'也是很重要. 例如, 買入correlation 相當高的 中國 及 亞洲, 只要在比例上控制,例如佔組合的30%,是無問題的.

又例如, 30%在亞洲區,同時買入 Templeton Asian Growth + Aberdeen Global Asia Pacific, 若是單看correlation 是不應該的, 這樣分散投資在2隻亞洲基金而非1隻反而可減低風險.

至於correlation, 其實很簡單的從Bloomberg又或Morningstar 取得, 大家真的要的話, 可pm我, 又或email我, 我可以幫你計.

若因為correlation問題而不考慮買入最佳的基金,長期下來,回報反而會減小.

^^

Ron38

[quote]

Oneness 寫道:

The funds in your portfolio has very high correlation with each other (see below). Therefore the risk cannot be diversified. You need to rearrange your portfolio to reduce the risk.

Ron38 寫道:

其實只要細心想便會發覺, 這樣的說法可以是對, 又可以是錯.

不是什麼也要'diversified'的. 例如買入一隻很穩定收息的公用股,而我買入2間,以至3間這樣的股票作為投資,是不是要'diversified' risk而去買其他sector 呢 ?

其實真的不是, 反而不是專買一隻公用股, 而將同一筆錢買幾隻同樣的公用股, 反而比買其他sector的股票, 例如banking sector 風險更低.

明不明白呢 ?! 我們要留意的, 是所投資的類別是什麼, 5 +

3988 不一定風險比 5 + 945高. 還有, oneness可不可提供 5 +3988的correlation 及 5+945的 correlation 呢 ?!

其實說真的, 不是計不到, 而是基金投資本身已分散大量風險了, 相信大家也聽過'系統風險'和'市場風險', 而硬要以correlation 去減低'市場風險', 這是不太可能的.

Correlation 用在不同的Asset Class是好好的工具, 但在同樣的Equity Class, 基本上用處不及以往的大.

這可參考The Intelligent Asset Allocator, 固中原因很簡單, 便是' 全球一體化'. 以往 歐洲, 亞洲, 日本, 印度以及美國, 市場有自己的獨立走勢, 所以用Correlation 是很有用的, 但問題是現在, 機本上全球的走勢也趨向一致(這是事實!!!) 美國大跌, 亞洲 + 歐洲也多數跟跌.

Ron38

[quote]

Oneness 寫道:

Your shares are all from the banking sector. This share portfolio is therefore not diversified. I would suggest you replace 939 and 3988 with other stocks or funds. 945 is a good choice for the long term.

Ron38 寫道:

再談Correlation 數字問題,有一個明顯的數字會出現, 就是'全球一體化'的出現, 使 基金 和 基金間(我即的是股票和股票, 即是同一個Asset Class) 的相關系數不斷上升.

(.... 其實, 感謝 神, 我的工作是很多時間進行研究的...)

剛剛出左份data, 大家參考下啦.

Value Partners Classic Fund Vs Fidelity European Growth.

Correlation :

02-06年 : 0.355 4年data

03-06年 : 0.579 3年 data.

這樣, 便是理想的一pair 嗎 ?

再看 :

04-06年 : 0.657 2年data

......

05-06件 : 0.824 1年data.

即是說, 若我們因為3年的correlation Data而選擇了 Value Partner Class + Fidelity European Growth, 但結果是, 原來最近一年也是所謂的'Highly correlated'.

換句話說, 有人問, 這2隻基金好嗎 ? 我可以答好(單看3年data), 也可以有另一位答你不好(用1至2年data)....

仍是果句, 數字, 可以有很多'玩'法, 但真正一隻基金的'成績'是無得改的. 希望大家對這方面多些了解.

^^

Ron38

再談.

sunshine0613 寫道:

Oneness,

I have some questions about the correlation of the funds I invested. Understand that China & Asia will have a high corelation as Asia included China. And there will be certain correlation between global with any other region no matter US, Europe, Asia or China. But can't understand why all these 4 will have high correlation as listed in the table.

What criteria will be used to generate the correlation figure? geographic factors? industrial factors? or what?

For the monthly investment for retirement, here are my info:

Aged 35 with a daughter of 2+ year old. I want to retire at 55 or latest 60. I guess I will die at around 80, that means 20-25 years to go after retired. I guess I need around HK$10k (at current value) per month after I retired.

I have around HK$180k (currently) accumulated in the MPF. And 2 (life+investment) insurance plans and other term life insurance plans. Cash+stock shares on hands around HK$200k. Mortage o/s amt of around HK$850k with o/s year of 13 years and property value is now around HK$1230k.

Ron38 寫道:

再談Correlation 數字問題,有一個明顯的數字會出現, 就是'全球一體化'的出現, 使 基金 和 基金間(我即的是股票和股票, 即是同一個Asset Class) 的相關系數不斷上升.

(.... 其實, 感謝 神, 我的工作是很多時間進行研究的...)

剛剛出左份data, 大家參考下啦.

Value Partners Classic Fund Vs Fidelity European Growth.

Correlation :

02-06年 : 0.355 4年data

03-06年 : 0.579 3年 data.

這樣, 便是理想的一pair 嗎 ?

再看 :

04-06年 : 0.657 2年data

......

05-06件 : 0.824 1年data.

即是說, 若我們因為3年的correlation Data而選擇了 Value Partner Class + Fidelity European Growth, 但結果是, 原來最近一年也是所謂的'Highly correlated'.

換句話說, 有人問, 這2隻基金好嗎 ? 我可以答好(單看3年data), 也可以有另一位答你不好(用1至2年data)....

仍是果句, 數字, 可以有很多'玩'法, 但真正一隻基金的'成績'是無得改的. 希望大家對這方面多些了解.

^^

Ron38

再談.

Ron38 寫道:

便是這樣, 若市場持續上升多一兩年, 基本上, 大部份'好'基金也會變成'Highly Correlated'.

若是如此, 這個Correlation也是不是真的很有用呢 ?! 再說, Correlation 在不同的Asset Class 是很有用的, eg. Hedge Fund + Equity + Bond, 因為大家有不同的走勢, 但在單單 Equity 方面, 真的效用不太大.

個人認為, 若真是考慮Correlation的話, 也是要留意 1年, 2年, 3年 等Correlation的數字.

另外, 因為這是統計學上的數字, 所以我們也不應單看Correlation 數字, 還要看當中的Standard Deviation. 原因是, 例如 VP vs Fidelity european Growth, 2年數字是 0.657, 當中有24個data, 但其中也可以有很大的差距, 所以, 一定要提出S.D.才可以完全.

換句話說, 例如基金表現, 我們不可單說回報, 而也要考慮S.D. (波幅)一樣.

如以上例子, 若VP vs Fidelity european Growth, 2年數字是 0.657, 而S.D是 0.3的話, 便又有問題了.

所以, 可以的話, 提出correlation 的同時, 也要提出S.D.

而我個人認為, Correlation 是要留意, 但因為考慮的地方太多, 果效不會很明顯.

反而, 如John C. Bogle所說的, 在強調'資產分配'的同時,也要留意, 以不同的渠道賺買基金的'成本'.

最後, 只想表達, 希望是和平的分享, 每人有不同的意見, 世界才會精彩.

^^

Ron38

[quote]

Oneness 寫道:

你這裡有些誤導,一般計correlation不會只用一至兩年的數據,因為在大牛市的時期,大部份股票基金都會同時升,所以correlation會增加,但當計算較長期的correlation時,便可計算出大家在不同市況時的相關性。

Value Partners Classic和Fidelity European Growth在02-06或03-06時相關性較低是因為當00-03熊市時Value Partners仍然錄得升幅,所以不會和Fidelity同時下跌。我們不是只看升市的相關性,亦要看跌市時的相關性,才能有效分散風險。

[quote]

Ron38 寫道:

再談Correlation 數字問題,有一個明顯的數字會出現, 就是'全球一體化'的出現, 使 基金 和 基金間(我即的是股票和股票, 即是同一個Asset Class) 的相關系數不斷上升.

(.... 其實, 感謝 神, 我的工作是很多時間進行研究的...)

剛剛出左份data, 大家參考下啦.

Value Partners Classic Fund Vs Fidelity European Growth.

Correlation :

02-06年 : 0.355 4年data

03-06年 : 0.579 3年 data.

這樣, 便是理想的一pair 嗎 ?

再看 :

04-06年 : 0.657 2年data

......

05-06件 : 0.824 1年data.

即是說, 若我們因為3年的correlation Data而選擇了 Value Partner Class + Fidelity European Growth, 但結果是, 原來最近一年也是所謂的'Highly correlated'.

換句話說, 有人問, 這2隻基金好嗎 ? 我可以答好(單看3年data), 也可以有另一位答你不好(用1至2年data)....

仍是果句, 數字, 可以有很多'玩'法, 但真正一隻基金的'成績'是無得改的. 希望大家對這方面多些了解.

^^

Ron38

再談.

發表於

發表於